Letter to MarketCrunch AI

Most "signals" are vibes. I want receipts. MarketCrunch AI publishes daily AI stock picks at ~5 PM PT. For each pick, I scan confidence + hit-rate, sanity-check momentum and volatility, then place in-the-money (ITM) options via limit order. The result is a fast, repeatable AI-assisted options trading workflow that keeps risk front-of-mind.

What you'll learn: a practical flow to filter picks, choose contracts, and exit with rules - plus four examples. Summary here, trade screenshots at bottom.

Why MarketCrunch AI?

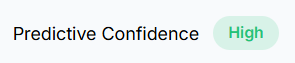

Clarity and context in one view: MarketCrunch AI uses a neural net engine to create explainable price estimate for next day price targets as well as next week's minimum and maximum price forecast. With each research report at a ticker level you get model's predictive confidence (by running thousand scenarios), prior hit rate on direction for both horizons short (7-day) and long (90-day), top three positive and negative factors leading to price estimate, backtested results (with Sharpe, drawdown, win-rate), and momentum/trend/volatility summary based on 19 most popular indicators (e.g. EMA, RSI, MACD, ADX, etc.)

This combo helps separate data-driven signals from FOMO.

The 5 PM Filter (2 min per ticker)

At 5PM Pacific, they publish 4–9 tickers as AI Picks by analyzing "350 millions+ data points" with predictive gain/loss for the next session. I go through each one and do a quick scan

Predictive confidence: Is 'High' - otherwise skip.

Hit-rate: Is it ≥ 50% on both 7-day and 90-day windows.

Weekly range bands: to see if the [max-current] and [current-min] price gaps and understand if the upward or downward potential, respectively aligns with daily estimate

Momentum & volatility sanity check: ensure technicals do not contract the daily price estimate

Context check: industry/theme, market cap, and whether news/sentiment agrees with the model's direction.

Biotech caveat: Small/mid-cap biotech options face halt & gap risk. Check for pending data readouts, AdComs, CRLs. Avoid holding into binary events unless that's your thesis.

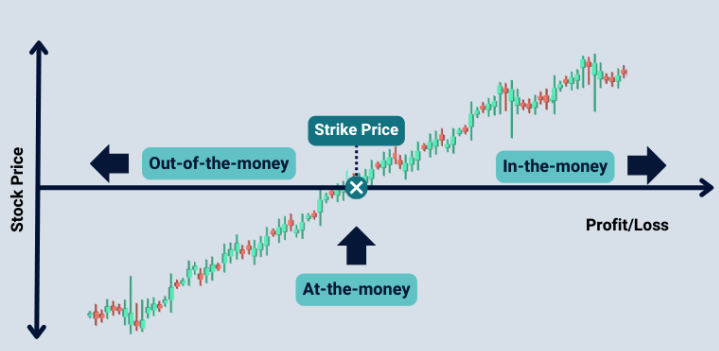

Picking the Option (ITM on purpose)

Direction:

- Bullish pick → Buy-to-Open ITM Call

- Bearish pick → Buy-to-Open ITM Put

Why ITM? ITM strikes put more premium into intrinsic value, so your option price tracks the underlying more and relies less on implied volatility. A ~0.50 delta gives a roughly coin-flip finish-ITM probability at current vols and reduces IV crush exposure vs OTM "lottos" (vega still matters).

Contract selection:

- Expiration: typically 2–4 weeks.

- Liquidity: bid/ask ≤ 5–10% of option price; OI ≥ 500 with same-day volume. Avoid micro-cap weeklies with $0.20-wide spreads on $0.60 options.

- Order type: Limit at/near mid; if spreads are wide, edge toward natural until filled.

- Delta ~0.50–0.60: responsive without being hyper-jumpy (rule-of-thumb probability of finishing ITM).

[Optional] IV & Event Guardrails

- IV percentile / IV rank: prefer entries when IV isn't at an extreme (unless you're trading the vol move).

- High IV or ugly spreads? Consider debit verticals to cap vega/theta and improve fills.

- Earnings / ex-div: don't open right before earnings unless that's the plan. (Early-exercise risk matters mostly for short calls near ex-div; we're long, so it's largely a non-issue.)

Liquidity & Sizing Rules

Liquidity checklist:

- Bid/ask ≤ 10% of price (≤ $0.05 if sub-$1 contracts)

- Underlying has adequate average daily dollar volume

Position sizing:

- 0.5–1.5% of account per trade (premium)

- 5–7% cap on total open options risk

- Watch correlations: don't load 3 tickers in the same factor bucket (e.g., small-cap bio)

Exit Playbook (numbers you can use)

- Profit-take: scale at +25–35%; leave a runner to +50–75% only if momentum + news agree

- Max loss: cut at –15–25% of premium or if the underlying violates your technical invalidation (e.g., closes below 20-EMA)

- Time stop: if no progress in 2–3 sessions and theta is accelerating, exit

Quick Examples

Trade labels used once for clarity: I Buy-to-Open ITM calls/puts and Sell-to-Close to exit. Not short calls.

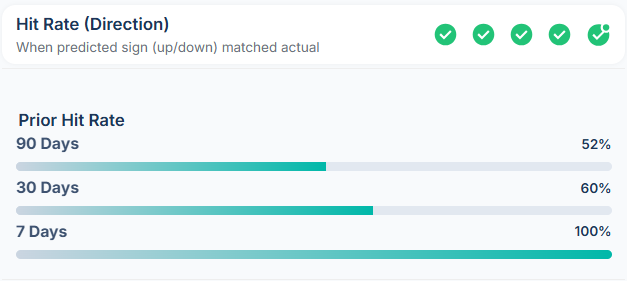

1) ABEO $5 Call

- Result: +25% on an ITM entry

- Entry: 9/26, 6:30 AM PDT • Exit: Not Yet

- Why: Cleared confidence/accuracy; no contradictory momentum.

- Action: Buy-to-Open ITM $5 Call, 10/17 expiry, 3 contracts, limit near mid.

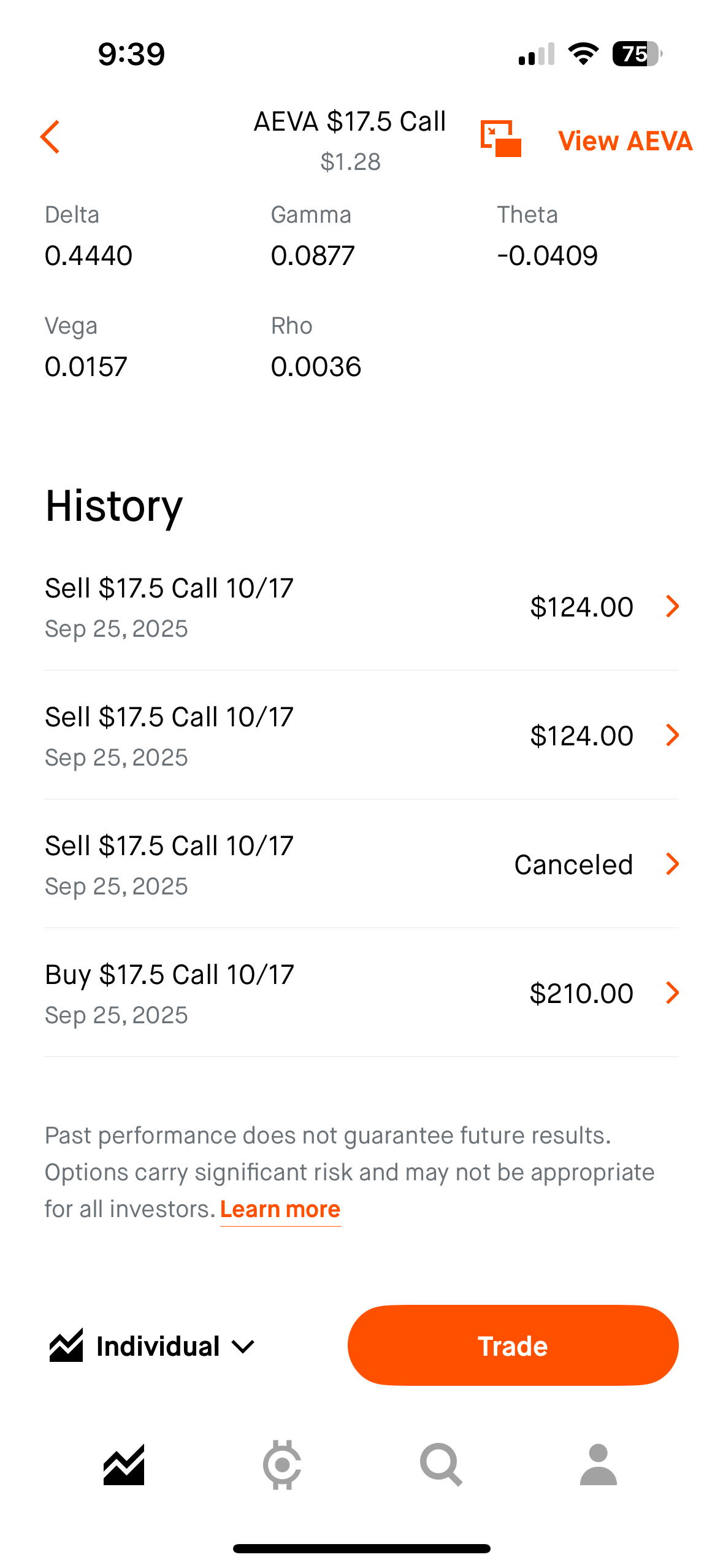

2) AEVA $17.5 Call - reading Greeks and spreads

- Result: +21%. Multiple partial closes near $124 credit; discipline > moonshots.

- Entry: 9/25, 6:30 AM PDT - Exit: 9/25, 9:38 AM PDT

- Why: Delta in range; spreads acceptable.

- Action: Worked limit orders around mid; scaled out on strength.

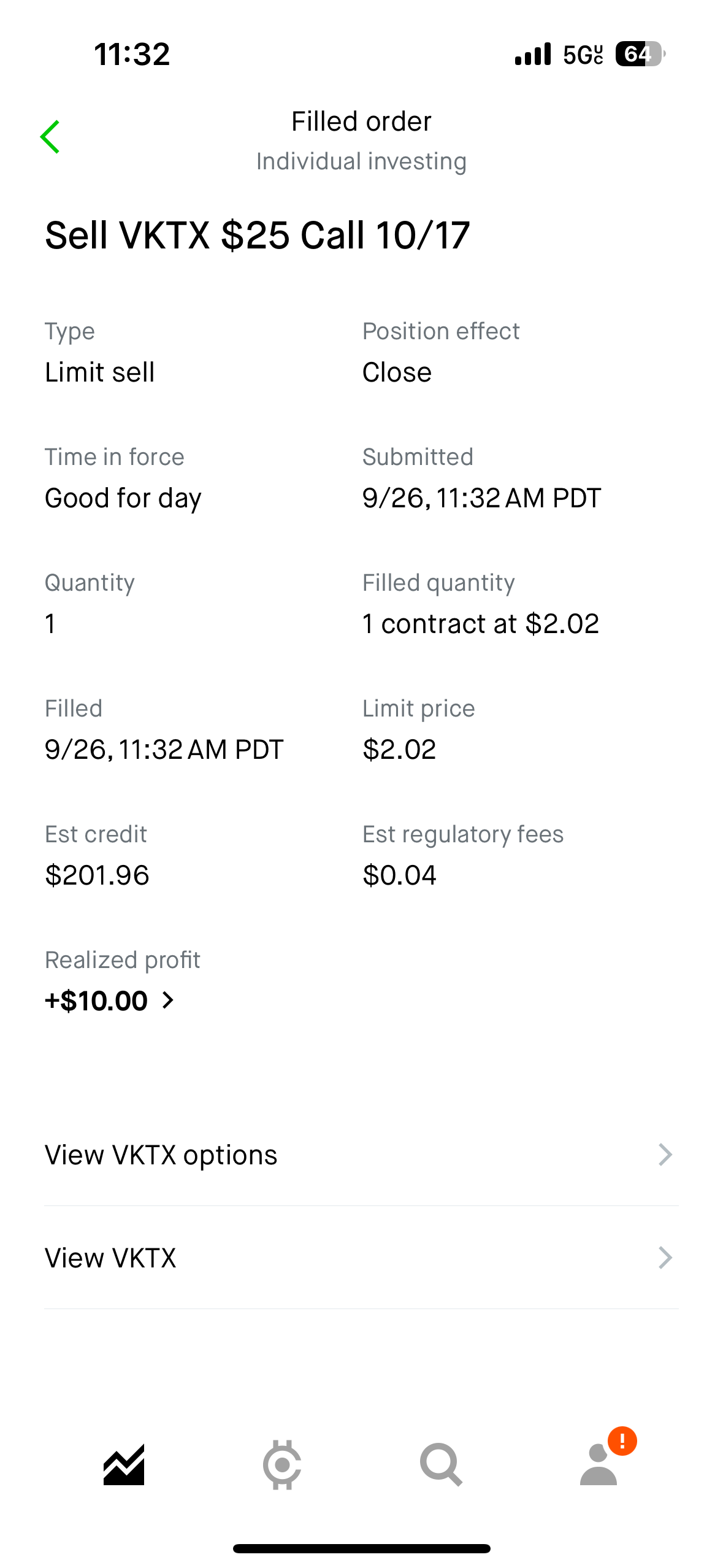

3) VKTX $25 Call - quick limit close

- Result: +5% ITM; intentional, risk-first exit.

- Entry: 9/26, 6:30 AM PDT • Exit: 9/26, 11:32 AM PT

- Why: Thresholds cleared; biotech momentum supportive.

- Action: Buy-to-Open ITM $25 Call → Sell-to-Close at $2.02 via limit as liquidity tightened.

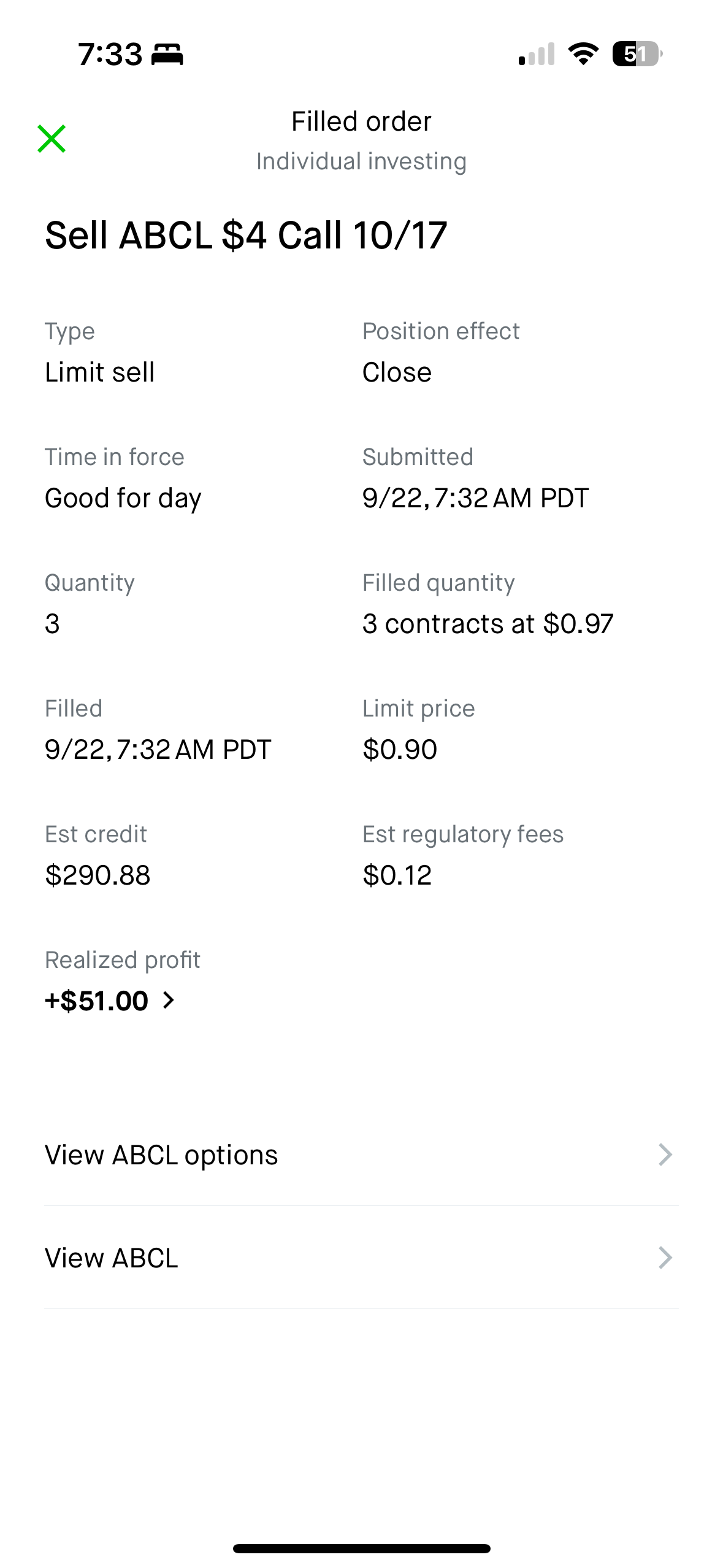

4) ABCL $4 Call - scaling exits on strength

- Result: +21% realized on that clip; repeatability > maxing every move. Screenshot alt: "ABCL ITM calls partial close around $0.97."

- Entry: 9/22, 6:30 AM PDT • Exit: 9/22, 7:32 AM PT

- Why: Filter checks cleared; analysis aligned.

- Action: Buy-to-Open ITM $4 Calls; later Sell-to-Close 3 contracts around $0.97 via limit.

Risk, Exits & Expectations (recap)

Options amplify outcomes. Size small, keep timeframes short, and decide exits before entries. MarketCrunch results are research, not advice; past performance ≠ future results.

Habits that help: avoid illiquid chains, respect theta (don't overstay weeklies), set alerts, re-check news/sentiment if a pick flips, review IV rank/percentile and the earnings calendar pre-entry. If IV is elevated or spreads > 10%, consider debit verticals to define risk and improve execution.

Next Steps

- See Next AI Picks → https://marketcrunch.ai/ai-picks (refreshes ~5p PT)

- Ticker Analysis referenced → VKTX, ABCL, ABEO, AEVA

FAQs

Q1: Are ITM calls or puts better for AI-driven entries? A: ITM options allocate more to intrinsic value, tracking the underlying better and reducing IV dependence vs OTM. Direction (call vs put) follows the model's signal.

Q2: How do I avoid IV crush? A: Skip pre-earnings entries unless trading the event, check IV rank/percentile, and consider debit verticals when IV is elevated.

Q3: What if spreads are wide? A: Use patient limit orders near mid or switch to a debit spread on tighter strikes to improve fills.

Q4: How big should a position be? A: Cap per-trade premium at 0.5–1.5% of account; cap total open options risk at 5–7%.

Disclaimer: This article is for education only. Nothing here is financial advice. Options involve risk and can lose 100% of premium.